Team DtL

How Coupons Can Help with Debt Management

In terms of personal finance, reaching financial freedom requires effective debt management. People are always looking for new and creative ways to get out of debt and move toward financial stability as they make their way through life. Remarkably, one such remedy is found in the domain of regular savings: coupons. In this in-depth tutorial, we explore the transformational potential of coupons and how they can be helpful tools on the path to debt management.

What are Coupons?

Coupons are promotional tools or vouchers that offer discounts, rebates, or other incentives to consumers to encourage them to purchase specific products or services. They typically feature a code or barcode that can be redeemed at the point of sale to receive the advertised discount or benefit.

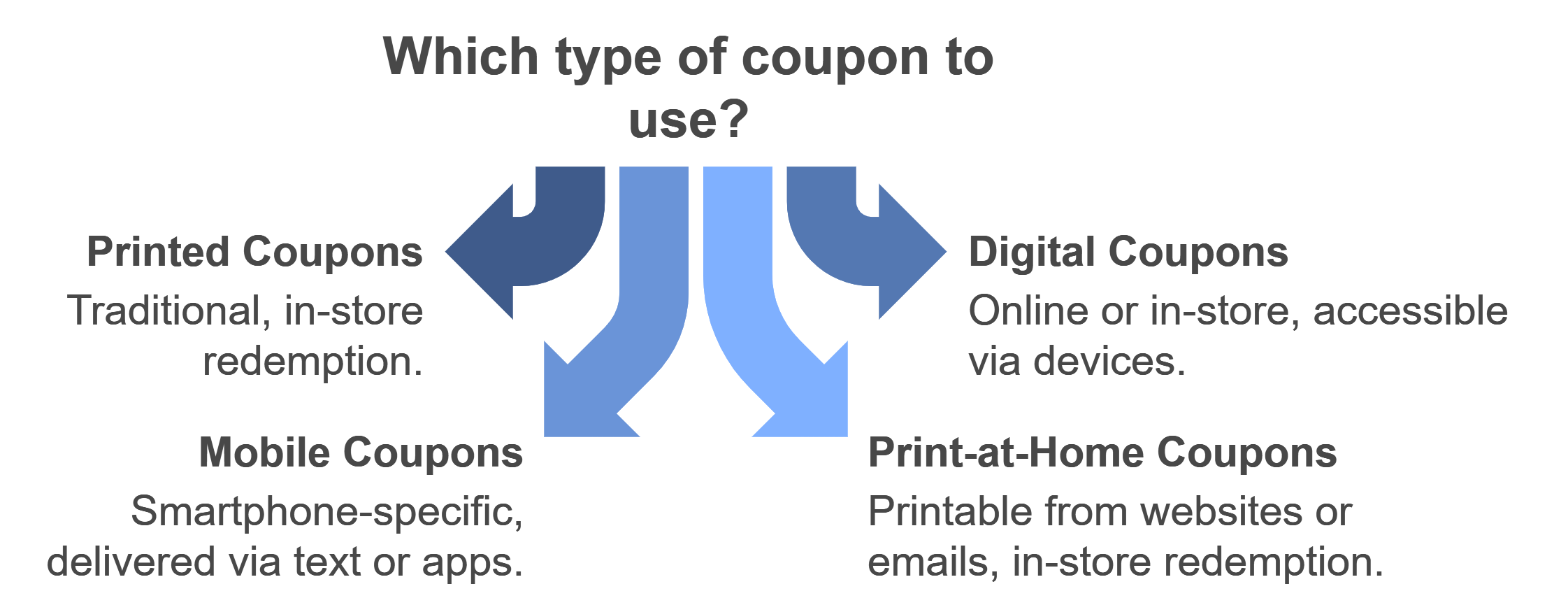

Coupons can take various forms, including:

- Printed Coupons: Traditionally, coupons were printed on paper and distributed through newspapers, magazines, direct mail, or in-store flyers. Consumers would cut out these paper coupons and present them at the checkout to receive the discount.

- Digital Coupons: With the rise of digital technology, coupons have become increasingly available in digital formats. Digital coupons can be found on websites, mobile apps, email newsletters, and social media platforms. They often feature unique codes or QR codes that can be scanned or entered electronically during online checkout or displayed on a mobile device for in-store redemption.

- Mobile Coupons: Mobile coupons are specifically designed for use on smartphones or other mobile devices. They can be received via text message, mobile apps, or mobile wallet platforms. Mobile coupons offer convenience and flexibility, allowing consumers to access and redeem discounts on the go.

- Print-at-Home Coupons: Some coupons are designed to be printed at home from websites or email promotions. Consumers can print these coupons on their home printers and present them at the store for redemption.

- Load-to-Card Coupons: Many grocery stores and retail chains offer load-to-card coupons, which are digital coupons that can be electronically loaded onto a shopper’s loyalty card or account. The reduction in price is applied automatically during the checkout process when the customer scans their loyalty card or provides their account details.

Coupons are typically issued by manufacturers, retailers, or service providers as part of marketing campaigns to attract customers, promote new products, boost sales, or reward loyal customers. Discounts are widely embraced and efficient methods for customers to economize on their routine expenditures while also enabling businesses to attract more visitors and boost their revenue.

Kinds of Coupons

Here’s a table outlining different kinds of coupons, along with brief descriptions:

| Type of Coupon | Description |

| Printed Coupons | Traditional paper coupons distributed through newspapers, magazines, or direct mail are typically clipped and redeemed in-store. |

| Digital Coupons | Coupons are distributed in digital format, accessible through websites, mobile apps, or email newsletters, for online or in-store use. |

| Mobile Coupons | Coupons are designed explicitly for use on smartphones or mobile devices and are often delivered via text message or mobile apps. |

| Print-at-Home Coupons | Coupons can be printed at home from websites or email promotions and redeemed in-store. |

| Load-to-Card Coupons | Digital coupons are loaded onto a shopper’s loyalty card or account for automatic redemption at checkout. |

| Manufacturer Coupons | Coupons issued by product manufacturers offer discounts on specific brands or products. |

| Store Coupons | Coupons issued by retailers or stores provide discounts on purchases made at specific locations. |

| Online Coupons | Coupons are distributed through e-commerce platforms or retailer websites, offering discounts on online purchases. |

| Loyalty Rewards | Discounts or rewards earned through loyalty programs or memberships are redeemable for future purchases. |

| Cashback Offers | Rebates or cash rewards earned on qualifying purchases are typically deposited into a designated account or platform. |

Understanding the Debt Dilemma

Before we explore the role of coupons in debt management, it’s essential to grasp the gravity of the debt dilemma facing millions worldwide.

From education loans to credit card balances and home mortgages, debt can significantly impede financial advancement and reduce overall well-being. Recent data reveals that the typical American family bears a significant debt load, emphasizing the need to identify lasting remedies swiftly.

The Rise of Couponing Culture

Amidst the quest for financial stability, the emergence of couponing culture has captured the attention of savvy consumers seeking to maximize savings. What began as a modest practice of clipping coupons from newspapers has evolved into a dynamic ecosystem fueled by digital platforms and mobile apps. Today, couponing has transcended its conventional boundaries, offering individuals unparalleled opportunities to save on everyday expenses.

To expand this section, we can delve into the history of couponing, tracing its origins from traditional paper coupons to the digital landscape we see today. We can explore the factors driving the popularity of couponing, such as economic downturns, increased accessibility through technology, and the desire for frugality and financial empowerment.

Harnessing the Power of Coupons

While coupons are commonly associated with grocery shopping and retail purchases, their potential extends far beyond mere discounts. When strategically employed, coupons can serve as valuable assets in debt management strategies. Here’s how:

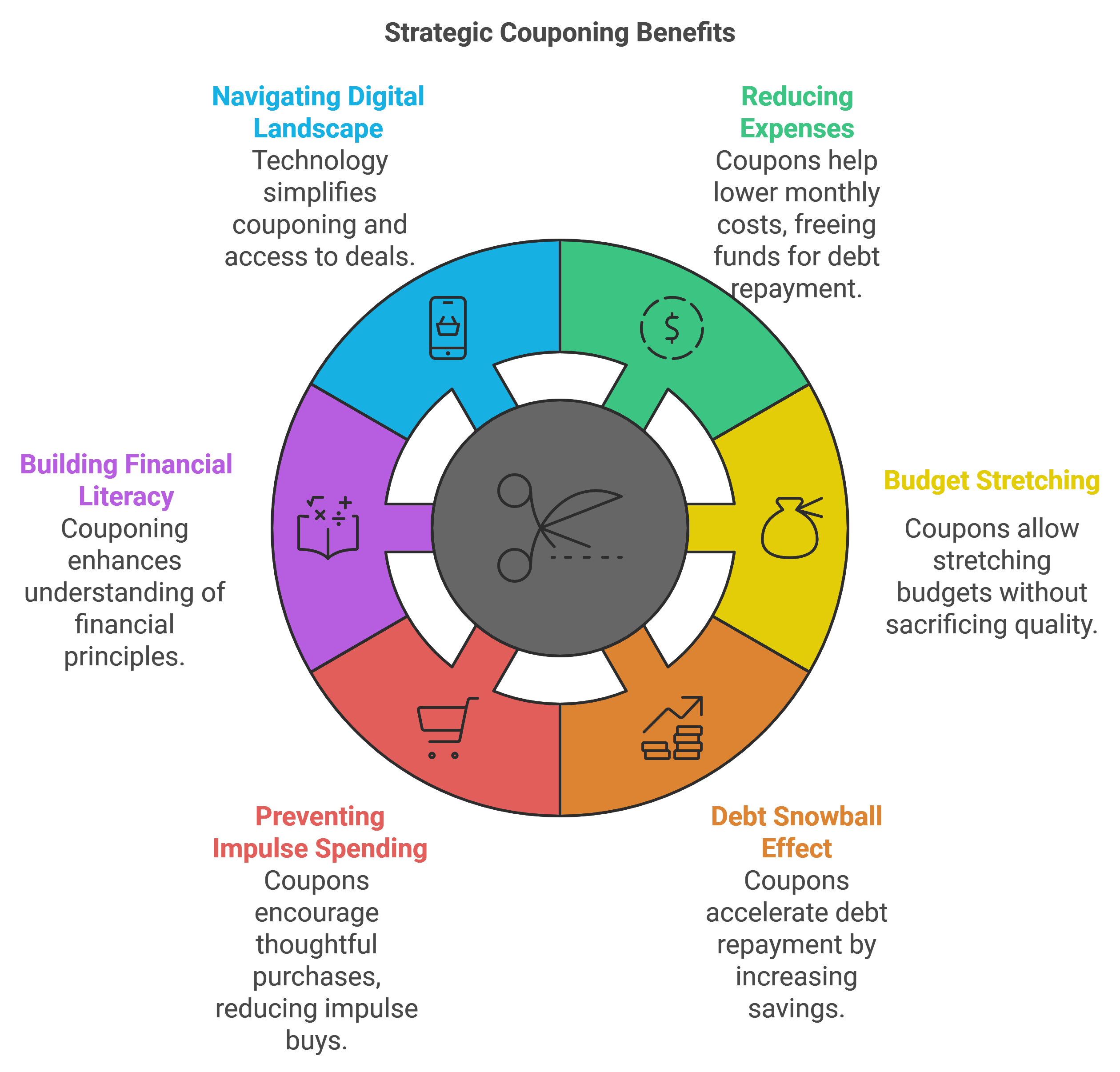

Reducing Expenses

At its core, couponing is about optimizing spending by capitalizing on discounts and promotions. By incorporating coupons into their purchasing habits, individuals can significantly lower their monthly expenses, freeing up additional funds to allocate toward debt repayment. Whether it’s groceries, household essentials, or entertainment expenses, the savings accrued through couponing can make a tangible difference in debt reduction efforts.

To expand this subsection, we can provide examples of everyday expenses where coupons can be utilized, such as groceries, dining out, entertainment, clothing, and household goods. We can also discuss the potential savings that can be achieved through strategic couponing and how these savings contribute to debt reduction goals.

Budget Stretching

For those with debt, maintaining a strict budget is a major challenge. Coupons act as catalysts for budget-stretching, allowing individuals to stretch their dollars further without sacrificing quality or convenience. By leveraging coupons to secure discounts on essential items, individuals can stay within budgetary constraints while still meeting their financial obligations.

Debt Snowball Effect

The debt snowball method, popularized by financial experts, emphasizes the importance of tackling smaller debts first to gain momentum in debt repayment. Coupons play a pivotal role in accelerating the debt snowball effect by amplifying savings on everyday purchases. As individuals consistently apply their couponing strategies and allocate the resultant savings towards debt repayment, they gradually gain traction in their journey toward financial freedom.

To use our Online Debt Snowball Calculator >>> CLICK HERE

Preventing Impulse Spending

Impulse spending is a common pitfall that can derail even the most meticulously crafted budget plans. Coupons serve as a deterrent to impulse spending by incentivizing thoughtful purchasing decisions. Instead of succumbing to spontaneous purchases, individuals are encouraged to prioritize items that offer the most outstanding value through coupon utilization. This mindful approach not only curtails unnecessary expenditures but also fosters disciplined financial habits conducive to debt management.

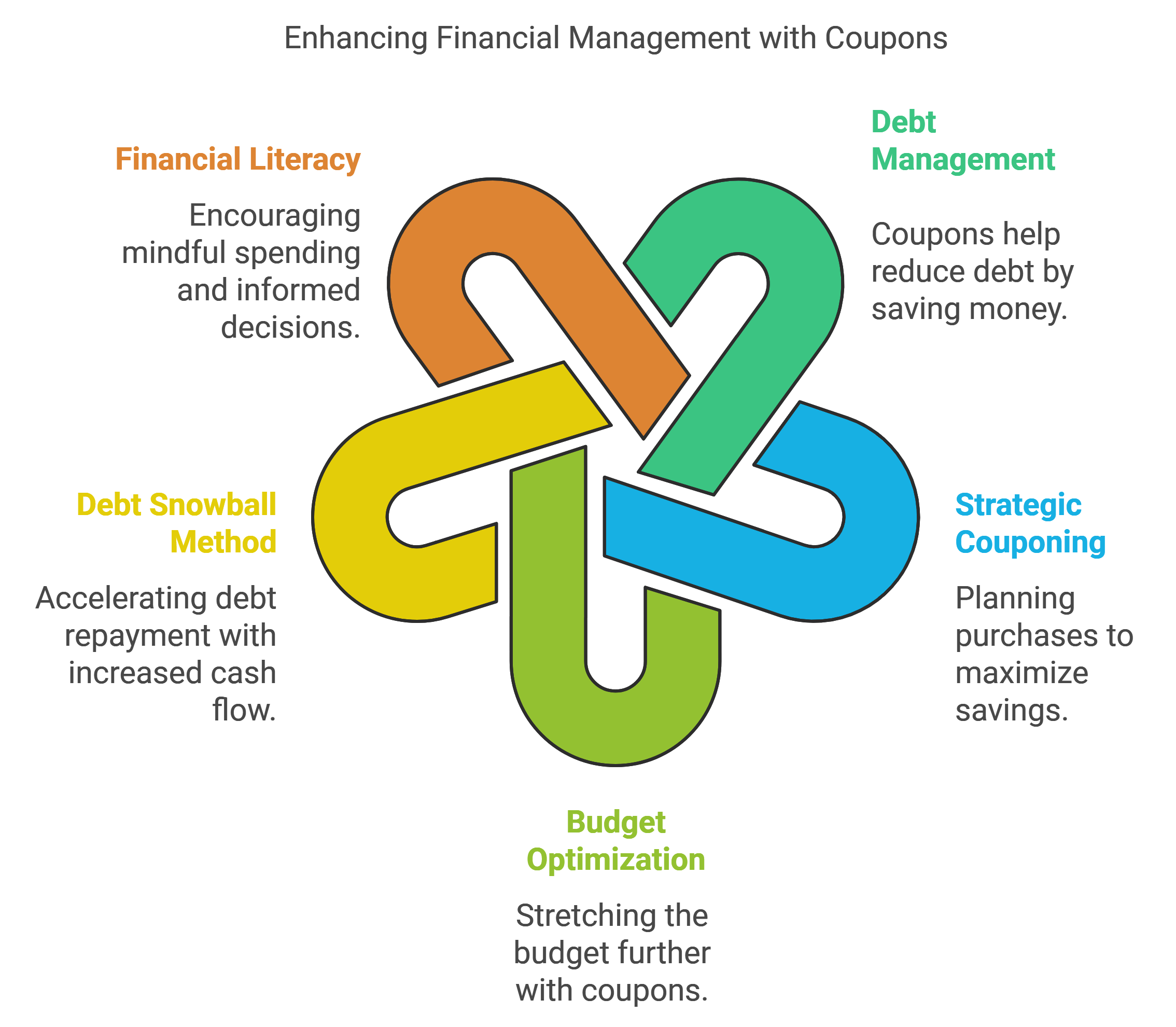

Building Financial Literacy

Beyond immediate cost savings, couponing fosters a deeper understanding of financial principles and consumer behavior. As people actively search for coupons, compare prices, and assess promotional deals, they acquire crucial financial literacy skills that enable them to make well-informed financial choices. This acquired knowledge forms a basis for enduring financial stability and equips individuals to tackle upcoming financial hurdles confidently.

Navigating the Digital Landscape

In today’s age of digital advancement, couponing has experienced significant changes. With the proliferation of couponing websites, mobile apps, and social media platforms, consumers have unprecedented access to a vast array of money-saving opportunities. By harnessing technology to their advantage, individuals can streamline the couponing process, discover exclusive deals, and stay abreast of promotional campaigns tailored to their preferences.

Various Uses of Coupons

Coupons offer versatile ways for consumers to save money and optimize their spending habits. Here are several diverse uses of coupons:

Grocery Shopping

Coupons are commonly used to save money on groceries, which are essential household expenses. Whether it’s for fresh produce, pantry staples, or household items, coupons provide discounts on a wide range of grocery products. Consumers can clip coupons from newspapers, print them from online sources, or use digital coupons from grocery store apps to lower their grocery bills.

Dining Out

Many restaurants offer coupons and promotional deals to attract customers. These coupons may offer discounts on meals, buy-one-get-one-free (BOGO) offers, or complimentary appetizers or desserts with the purchase of an entrée. By using dining coupons, individuals and families can enjoy meals at restaurants while saving money on their dining expenses.

Online Shopping

E-commerce platforms and retailers often provide coupon codes that customers can apply during online checkout to receive discounts on their purchases. These online coupons may offer percentage discounts, dollar-off savings, free shipping, or other incentives. Online customers can get discounts on a range of goods and services by using a coupon code at the time of checkout.

Retail Purchases

Coupons are frequently used in retail stores to offer discounts on clothing, electronics, home goods, and other merchandise. Retail coupons may be distributed through flyers, catalogs, or email newsletters, and they can provide significant savings on both regular-priced and clearance items. By presenting coupons at the register or entering promo codes online, shoppers can enjoy discounted prices on their retail purchases.

Entertainment

Coupons can be used to save money on entertainment expenses, including movie tickets, live events, theme park admissions, and recreational activities. Entertainment coupons may offer discounts on admission fees, concession purchases, or package deals for multiple attractions. By taking advantage of these coupons, individuals and families can enjoy leisure activities without overspending on entertainment costs.

Travel and Accommodations

Travel coupons can help travelers save money on transportation, accommodations, and other travel-related expenses. Coupons may offer discounts on airline tickets, hotel stays, rental cars, or vacation packages. By seeking out travel deals and using coupons, travelers can reduce the total expense of their trips and vacations.

Health and Wellness

Coupons are also available for health and wellness products and services, such as vitamins, supplements, gym memberships, and spa treatments. These coupons may provide discounts on purchases, free trials, or special promotions. By using these coupons, individuals can prioritize their health and well-being while staying within their budget.

Services

Discount vouchers are available for a range of services, such as car maintenance, house cleaning, pet care, and expert advice. These vouchers might provide price cuts, bundled deals, or special rates for first-time clients. Utilizing these vouchers allows people to access essential services while keeping their costs down.

Coupons offer consumers a multitude of opportunities to save money on everyday purchases, activities, and services. By being resourceful and proactive in seeking out coupons, individuals can maximize their savings and make their money go further. Coupons offer significant savings across various expenses like groceries, dining, online purchases, and travel, aiding individuals in reaching their financial targets and enhancing their general well-being.

Tips on How to Utilize Coupons

Here are some practical tips on how individuals can utilize coupons to manage or reduce their debt effectively:

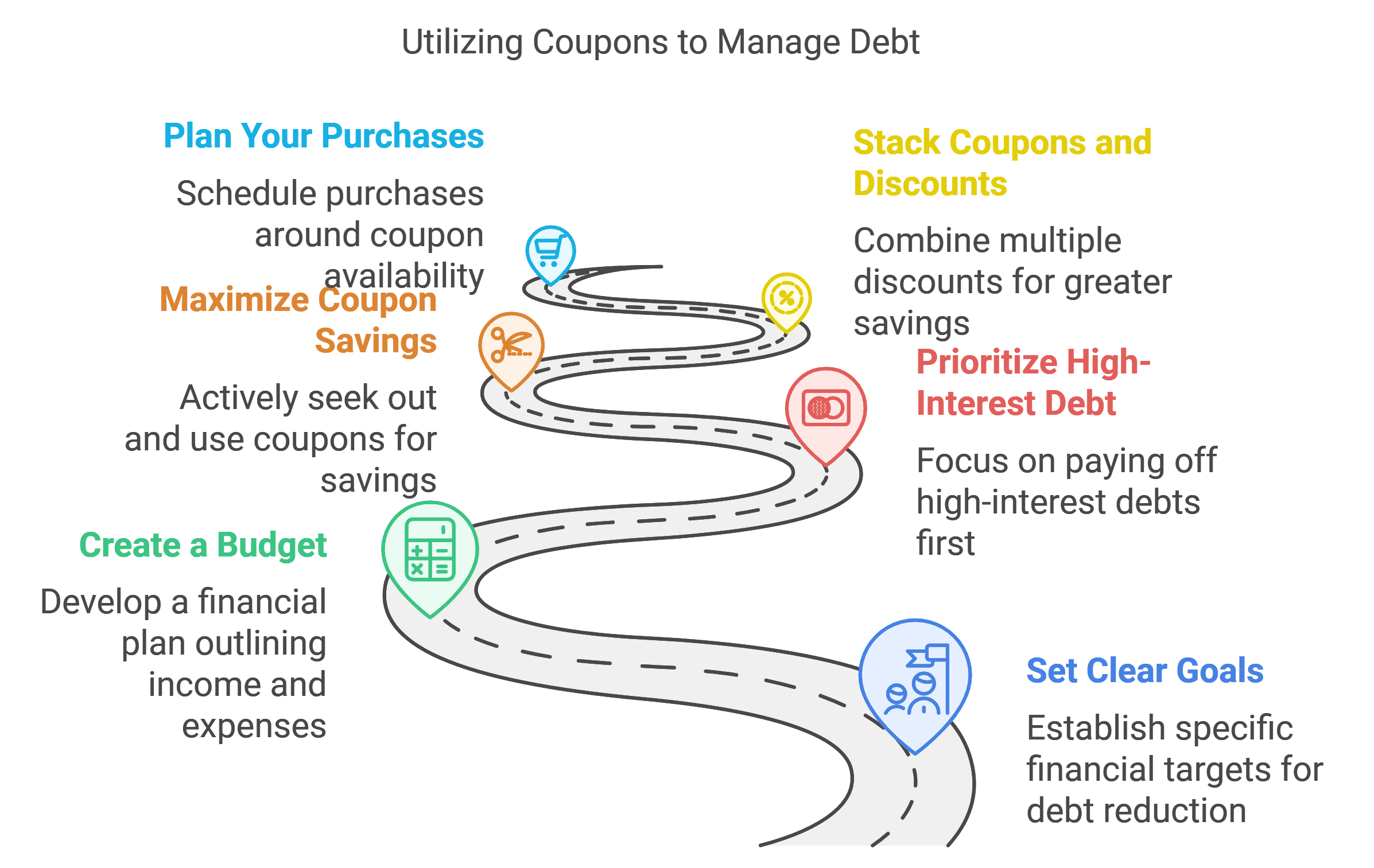

- Set Clear Goals: Start by setting clear financial goals, including specific targets for debt reduction. Determine how much debt you want to pay off and by when. Maintaining a clear objective will keep you driven and concentrated on your efforts to pay off your debts.

- Create a Budget: Create a thorough financial plan outlining your income, spending, and existing debts. Identify areas where you can cut costs to allocate more funds to repay debts. Use coupons to reduce the costs of essential purchases, such as groceries, household items, and entertainment.

- Prioritize High-Interest Debt: Eliminate high-interest debt, like outstanding credit card balances, since it can increase and impede your financial advancement. Allocate extra funds to pay off high-interest debt while making minimum payments on other debts.

- Maximize Coupon Savings: To maximize your savings, be proactive in seeking out coupons and promotional deals. Utilize a variety of sources, including newspapers, online coupon websites, mobile apps, and retailer promotions. Search for discounts or vouchers for products you frequently buy to lower your costs for groceries and household items.

- Stack Coupons and Discounts: Take advantage of opportunities to stack coupons and discounts for even more significant savings. Combine manufacturer coupons with store promotions, loyalty rewards, and cashback offers to maximize your savings on purchases. Look for opportunities to double or triple your coupon savings by pairing them with existing discounts.

- Plan Your Purchases: To optimize your savings, plan your purchases around coupon availability and promotional periods.

- To get the greatest discounts, take advantage of seasonal sales, clearance events, and holiday promotions. Consider stocking up on non-perishable items when prices are lowest to maximize your savings over time.

- Track Your Savings: Monitor your progress and stay motivated by tracking your coupon-related savings. Create a system for organizing your coupons and tracking your expenses to ensure you’re maximizing your savings potential. Use couponing apps or spreadsheets to track your savings over time and adjust your strategies as needed.

- Stay Consistent: Consistency is critical to couponing and debt repayment. Incorporate couponing into your regular schedule and maintain dedication to your debt repayment objectives. Acknowledge and rejoice in your achievements as you progress while keeping your sights fixed on the lasting advantages of achieving financial freedom.

Maximizing Couponing Success

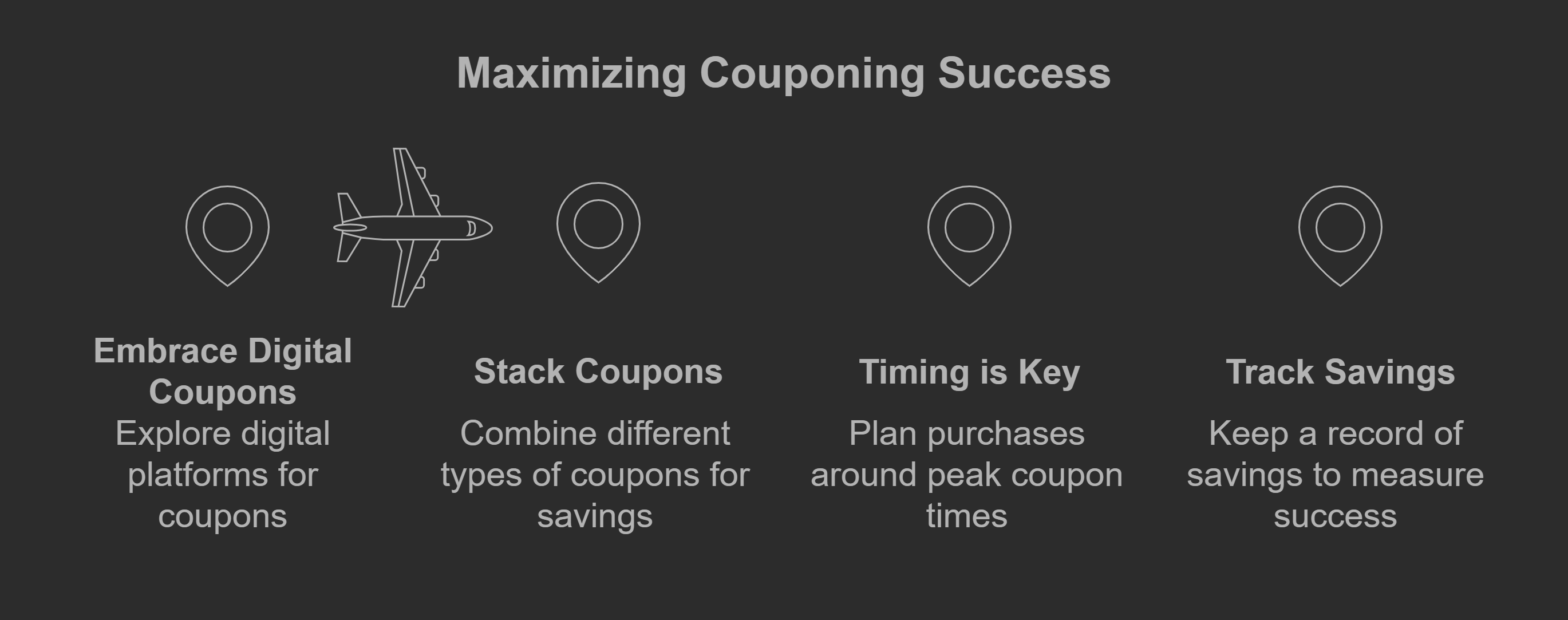

While coupons undeniably offer substantial benefits in debt management, maximizing their effectiveness requires a strategic approach. Here are some tips to optimize couponing success:

- Embrace Digital Coupons: Explore the multitude of digital couponing platforms available, including dedicated couponing apps, retailer websites, and cashback portals. By digitizing your couponing efforts, you can access a more comprehensive selection of deals and streamline the redemption process.

- Stack Coupons: Take advantage of coupon stacking opportunities by combining manufacturer coupons with store promotions or loyalty rewards. This synergistic approach allows for maximum savings on eligible purchases, amplifying the impact on debt reduction efforts.

- Timing is Key: Strategically time your purchases to coincide with peak coupon availability and promotional periods. By planning and leveraging seasonal discounts or clearance sales, you can capitalize on optimal savings opportunities.

- Track Savings: Maintain a comprehensive record of your couponing endeavors to track savings over time. By measuring the savings generated from your coupons and keeping track of your progress, you acquire valuable knowledge about how well your couponing methods are working and can make adjustments as needed.

Key Takeaways:

- Coupons as Debt Management Tools: Coupons can be powerful tools for managing and reducing debt by helping individuals save money on everyday expenses.

- Strategic Couponing: Strategic couponing involves planning purchases, maximizing savings opportunities, and allocating coupon-related savings toward debt repayment.

- Budget Optimization: Incorporating coupons into budgeting strategies can stretch your budget further, allowing you to allocate more funds towards debt repayment.

- Debt Snowball Method: Utilizing coupons can accelerate the debt snowball method by increasing cash flow and expediting debt repayment.

- Financial Literacy: Couponing fosters financial literacy by encouraging mindful spending, comparison shopping, and informed financial decision-making.

Frequently Asked Questions (FAQs)

How do coupons help with debt management?

Coupons help with debt management by reducing expenses, stretching budgets, and freeing up additional funds for debt repayment.

What types of expenses can coupons help with?

Coupons can help with a wide range of costs, including groceries, dining out, retail purchases, entertainment, travel, services, and more.

How can I maximize savings with coupons?

To maximize savings with coupons, utilize a variety of sources, stack coupons and discounts, plan purchases around promotions, and track your savings over time.

Can couponing really affect debt repayment?

Yes, couponing can significantly affect debt repayment by increasing cash flow, reducing expenses, and accelerating debt payoff.

Are there any risks or downsides to couponing?

While couponing can offer substantial savings, it’s essential to avoid overspending or purchasing unnecessary items just because you have a coupon. Be mindful of expiration dates, terms and conditions, and any potential fees associated with coupon use.

Additional Resources:

- Coupon Websites and Apps

- RetailMeNot (https://www.retailmenot.com/)

- Coupons.com (https://www.coupons.com/)

- Honey (https://www.joinhoney.com/)

- Rakuten (https://www.rakuten.com/)

- Financial Literacy Resources

- National Endowment for Financial Education (NEFE): https://www.nefe.org/

- MyMoney.gov: https://www.mymoney.gov/

- Consumer Financial Protection Bureau (CFPB): https://www.consumerfinance.gov/

- Debt Repayment Tools and Calculators

- Debt Snowball Calculator: https://www.nerdwallet.com/article/finance/debt-snowball-calculator

- Debt Payoff Planner: https://www.creditkarma.com/calculators/debt-payoff

- Couponing Guides and Articles

- The Krazy Coupon Lady: https://thekrazycouponlady.com/

- Money Crashers – Beginner’s Guide to Coupons: https://www.moneycrashers.com/coupons-for-beginners-guide/

Conclusion

Striving for financial independence involves valuing each saved dollar as a significant stride toward breaking free from the chains of debt. By harnessing the transformative power of coupons, individuals can embark on a pragmatic and empowering journey of debt management. Through strategic couponing practices, budget optimization, and financial literacy cultivation, individuals can chart a course toward a brighter economic future characterized by stability, security, and abundance. Embrace the potential of coupons as catalysts for change and unlock the path to financial freedom today.

Finding Peace and Financial Freedom: A Prayer for a Debt-Free Life

Amidst the hectic pace of contemporary life, financial concerns frequently occupy our thoughts. The weight of debt, which includes credit card debt, mortgages, school loans, and unforeseen medical expenses, may be debilitating. Many people seek comfort and direction from prayer during difficult financial times. A prayer for debt-free living is a sincere declaration of confidence in a higher power to bring comfort and support during difficult times, not just a request for financial gain.

Understanding the Power of Prayer

In today’s fast-paced world, where the relentless pursuit of material wealth often overshadows spiritual fulfillment, prayer emerges as a sanctuary of solace and tranquility. It transcends religious boundaries, resonating with individuals across cultures and beliefs. Whether it’s the quiet contemplation of a solitary soul or the communal gathering of worshippers, prayer serves as a timeless practice that connects humanity with the divine.

Essentially, prayer is a meaningful conversation between the divine and the mortal, not merely a string of words spoken into space. Imagine a sacred space where people can freely open up about their deepest fears, hopes, and aspirations without any fear of judgment. This space, often found in prayer, offers solace as individuals realize they’re not alone in their trials. Whether they believe in God, the universe, or some cosmic force, they find comfort in the idea that something greater listens to them with kindness.

Prayer isn’t just about seeking help; it’s a journey inward. Being prompted to consider our values, beliefs, and aspirations can help us gain a more profound knowledge of ourselves and our place in the world. It’s similar to going on a mission to discover our purpose and level of self-awareness, probing deeper truths by delving into our innermost selves.

Furthermore, prayer is a healing practice for the heart and intellect as well as for the soul. Regular prayer has been shown in studies to reduce stress, anxiety, and depression while promoting serenity and peace. It makes room for mindfulness, allowing us to put our problems aside and discover contentment in the here and now.

But prayer isn’t a solitary act—it connects us. When we pray for ourselves, we naturally extend our thoughts to others, fostering empathy and unity with those facing similar struggles. It’s this interconnectedness that fuels acts of kindness, generosity, and justice, making prayer a powerful force for positive change in society.

Sample Prayer

“Dear [Divine Source/Higher Power/God],

I come before you with a humble heart, seeking your guidance and blessings on my journey toward financial freedom and abundance. In the midst of uncertainty and worry, I turn to you for strength and reassurance, knowing that you are always present, ready to guide me toward a brighter future.

I would like your wisdom to help me make sound financial decisions, manage my resources wisely, and use them for the highest good of myself and others. Please grant me the courage to release any fears or doubts that may be holding me back from experiencing true prosperity and abundance in all areas of my life.

Fill my heart with gratitude for the blessings I already possess, and open my eyes to the abundance that surrounds me each day. Please help me cultivate a spirit of generosity and compassion, knowing that the more I give, the more I receive in return.

Guide me toward opportunities for growth and prosperity, and lead me along the path of financial freedom with grace and ease. May my actions be aligned with your divine will, and may I always trust in your timing and provision.

I surrender my worries and fears to you, knowing that you are the ultimate source of all abundance and prosperity. Thank you for your love, your guidance, and your infinite blessings.

Amen.”

The Spiritual Approach to Financial Freedom

In a world where material wealth is often equated with success and happiness, the spiritual approach to financial freedom offers a profound alternative perspective. It transcends the mere accumulation of possessions and monetary assets, emphasizing instead the alignment of financial goals with more profound spiritual principles.

At its core, the spiritual approach to financial freedom recognizes that true wealth encompasses more than just material abundance—it encompasses spiritual fulfillment, emotional well-being, and a sense of purpose. It invites individuals to reevaluate their relationship with money, shifting from a mindset of scarcity and lack to one of abundance and gratitude.

At the core of this perspective lies the idea that achieving financial success isn’t solely reliant on external measures like income or possessions but also on an individual’s internal mindset and well-being. It acknowledges the interconnectedness of mind, body, and spirit, recognizing that true abundance arises from a harmonious alignment of these aspects of the self.

Moreover, the spiritual approach to financial freedom encourages individuals to view money as a tool for personal and collective growth rather than an end in itself. It invites them to cultivate a mindset of generosity and service, recognizing that the more they give, the more they receive in return.

In essence, the spiritual approach to financial freedom is grounded in the understanding that material wealth is fleeting and impermanent, while spiritual wealth endures for eternity. It encourages individuals to seek fulfillment not in external possessions but in the richness of their inner lives—their relationships, their passions, and their connection to something greater than themselves.

Practically, this approach may involve practices such as mindfulness, gratitude, and conscious consumption. It invites individuals to examine their spending habits and financial priorities, discerning what truly brings them joy and fulfillment. It encourages them to align their economic decisions with their values and aspirations, thereby fostering a sense of coherence and purpose in their financial lives.

Ultimately, the spiritual approach to financial freedom is about reclaiming sovereignty over one’s economic destiny. It empowers individuals to transcend the limitations of the material world and embrace a more expansive vision of prosperity—one that is rooted in spiritual wisdom, compassion, and abundance. By adopting this approach, individuals can cultivate a more profound sense of fulfillment and purpose in their financial lives, leading to greater peace, joy, and freedom.

Benefits of Prayer

Prayer is a timeless practice that spans cultures, religions, and belief systems. Beyond its spiritual significance, prayer offers a myriad of benefits that positively impact mental, emotional, and physical well-being. Here are some of the critical benefits of prayer:

Stress Reduction

Studies have demonstrated that prayer can decrease stress by encouraging a state of relaxation and calmness. Participating in religious practices can assist people in easing tension, quieting their thoughts, and discovering inner serenity amid life’s trials.

Improved Mental Health

Regular prayer practice is associated with improved mental health outcomes, including reduced symptoms of anxiety, depression, and mood disorders. Prayer offers a feeling of consolation and peace, providing comfort during moments of emotional turmoil.

Enhanced Emotional Resilience

Prayer fosters emotional resilience by providing a coping mechanism for dealing with adversity and setbacks. It promotes individuals to openly share their emotions and worries, fostering improved emotional health and steadiness.

Increased Gratitude

Prayer cultivates a spirit of gratitude by prompting individuals to reflect on their blessings and express thanks for the abundance in their lives. Gratitude has been linked to numerous psychological benefits, including increased happiness and life satisfaction.

Sense of Purpose

Prayer helps individuals connect with their sense of purpose and meaning in life. It offers a chance for self-examination and contemplation, leading to a better understanding of one’s beliefs, objectives, and ambitions.

Social Connection

Prayer often involves communal worship and shared rituals, fostering a sense of belonging and social connection. Participating in prayer communities can strengthen relationships, build support networks, and promote feelings of unity and solidarity.

Physical Health Benefits

Praying may have positive effects on physical health, including lower blood pressure, reduced risk of heart disease, and enhanced immune function. Prayer is thought to activate the body’s relaxation response, leading to improved overall health and well-being.

Improved Relationships

Prayer promotes empathy, compassion, and forgiveness, which are essential components of healthy relationships. By fostering a sense of interconnectedness and goodwill towards others, prayer can strengthen bonds and resolve conflicts.

Increased Resilience

Prayer instills hope and optimism, even in the face of adversity. It promotes the idea of relying on divine guidance and letting go of worries by entrusting them to a higher authority. This practice fosters increased resilience and determination, particularly during challenging moments.

Spiritual Growth

Ultimately, prayer is a pathway to spiritual growth and transformation. It deepens individuals’ connection with the divine, fosters a sense of awe and wonder, and nourishes the soul. Through prayer, individuals can cultivate virtues such as faith, humility, and compassion, leading to greater spiritual fulfillment and enlightenment.

Prayer provides numerous advantages that go beyond the boundaries of just spiritual aspects. From stress reduction to improved mental health and enhanced relationships to increased resilience, prayer has the power to impact every aspect of human well-being positively. As a timeless practice that transcends cultural boundaries, prayer continues to serve as a source of strength, comfort, and inspiration for countless individuals around the world.

Trusting in Divine Guidance

In moments of financial turmoil, faith serves as a guiding light, illuminating pathways out of darkness. The prayer for a debt-free life reflects an unwavering trust in divine providence. It acknowledges that while humans may plan their course, it is the divine hand that ultimately directs their steps. This surrender to a higher power fosters resilience in the face of adversity, instilling hope where despair once reigned.

Surrendering to the Will of the Universe

True surrender is an act of profound humility and acceptance. It requires relinquishing control and embracing uncertainty with open arms. The prayer for a debt-free life invites individuals to release their attachments to material possessions and outcomes. In doing so, they discover a newfound freedom, unencumbered by the weight of worldly concerns. This surrender opens the door to unexpected blessings and serenity beyond measure.

Finding Gratitude in Times of Need

Gratitude is a transformative force that transcends circumstance. Even in the depths of financial hardship, there is always something to be thankful for. The prayer for a debt-free life encourages individuals to shift their focus from scarcity to abundance. By cultivating a spirit of gratitude, they awaken to the richness of life’s blessings, both big and small. This shift in perspective fosters resilience and empowers individuals to weather life’s storms with grace.

Taking Action with Faith

Faith without action is like a ship without a rudder—adrift and directionless. The prayer for a debt-free life calls individuals to marry their faith with practical steps toward financial freedom. This could include developing a budget, consulting with financial experts, or exploring additional sources of income. By taking proactive measures, individuals demonstrate their commitment to co-creating their financial destiny with the divine.

Embracing the Journey Toward Financial Freedom

Financial freedom is not merely a destination but a transformative journey of self-discovery and empowerment. Along the way, individuals may encounter obstacles and setbacks, but these challenges are opportunities for growth. The prayer for a debt-free life invites individuals to embrace the journey wholeheartedly, trusting in the wisdom of divine timing. With each step forward, they move closer to realizing their vision of a debt-free existence—a testament to the power of faith and perseverance.

Here’s a table summarizing key aspects of prayer for a debt-free life:

| Aspect | Description |

| Purpose | I am seeking guidance, support, and comfort from a higher power in the journey toward financial freedom. |

| Spiritual Approach | Emphasizes aligning financial goals with more profound spiritual principles, viewing money as a tool for personal growth and service rather than an end in itself. |

| Benefits |

|

| Importance of Surrender | They are surrendering worries and fears to divine guidance, trusting in a higher power’s provision and timing for financial blessings. |

| Practical Action | I am combining prayer with practical steps toward financial freedom, such as budgeting, seeking financial advice, and increasing income streams. |

| Community and Support | You are engaging in communal prayer and seeking support from spiritual communities for encouragement and solidarity in the journey toward financial well-being. |

| Persistence and Trust | It is maintaining faith and perseverance in prayer, trusting in divine guidance and provision even in the face of financial challenges. |

| Personalization and Faith | Individuals tailor prayers to reflect their own beliefs and desires, express sincere feelings, and nurture a strong sense of faith and connection with the spiritual realm. |

Here’s a concise overview of the key elements and practices associated with praying for a debt-free life. It emphasizes how prayer impacts spiritual, emotional, and practical aspects, aiding in attaining financial stability.

Key Takeaways:

- Prayer for Financial Freedom: Prayer serves as a powerful tool for finding peace, guidance, and support on the journey toward financial freedom. It is a spiritual practice that transcends material concerns, fostering a deeper connection with a higher power and providing solace in times of economic stress.

- Spiritual Approach to Finances: The spiritual approach to finances emphasizes aligning financial goals with deeper spiritual principles. It encourages individuals to view money as a tool for personal growth and service rather than an end in itself. By cultivating gratitude, generosity, and mindfulness, individuals can foster a sense of abundance and fulfillment in their financial lives.

- Benefits of Prayer: Prayer offers a myriad of benefits for mental, emotional, and physical well-being. It reduces stress, enhances emotional resilience, fosters gratitude, and strengthens relationships. Moreover, prayer promotes spiritual growth and connection with the divine, leading to greater inner peace and fulfillment.

FAQs

What is the purpose of a prayer for financial freedom?

A prayer for financial freedom is a spiritual practice that helps individuals align their financial goals with deeper values and principles. It is a means of seeking guidance, comfort, and support from a higher power in times of financial uncertainty.

How does prayer contribute to financial well-being?

Prayer promotes emotional resilience, reduces stress, and fosters gratitude—all of which contribute to overall financial well-being. By cultivating a sense of trust in a higher power and surrendering worries to divine guidance, individuals can navigate financial challenges with greater clarity and peace of mind.

Is there scientific evidence supporting the benefits of prayer?

While prayer is often associated with spiritual beliefs, numerous studies have documented its positive effects on mental, emotional, and physical health. Research suggests that regular prayer practice can reduce stress, improve emotional well-being, and even enhance physical health outcomes.

Additional Resources:

- Books

- “The Power of Prayer: Enhance Your Life and Improve Your Financial Well-Being” by Catherine Ponder

- “The Secret to Financial Freedom Through Prayer” by Michael A. Lane

- Websites

- Studies and Articles

- Koenig, H. G., et al. (2001). “Prayer and Depression.” Journal of Religion and Health, 40(4), 377–388.

- In their paper “The Role of Religion and Spirituality in Mental and Physical Health,” which was published in Current Directions in Psychological Science, Seybold and Hill (2001) examine the effects of spirituality and religion on mental and physical health. They delve into how these aspects influence various facets of well-being, presenting insights into the complex interplay between spirituality, religion, and health outcomes.

Conclusion

In a world consumed by materialism and consumerism, the prayer for a debt-free life offers a counter-narrative of spiritual abundance and fulfillment. It emphasizes the idea that real wealth isn’t found in material possessions but rather in the depth and richness of one’s character and inner self. Through prayer, individuals find solace, guidance, and strength to navigate life’s financial challenges with grace and gratitude. As they align their actions with divine will, they embark on a journey of self-discovery and empowerment, embracing the path to financial freedom with unwavering faith and determination.

Practical Strategies to Avoid Bank of America Core Checking Maintenance Fee

In today’s financial landscape, understanding the fee structures associated with banking services is essential for responsible economic management. One fee that many Bank of America (BoA) customers encounter is the core checking maintenance fee. This detailed handbook will explore the fundamental concept of checking maintenance fees, the reasons behind their imposition, and effective methods to steer clear of them. Whether you’re a current BoA customer or considering opening a core checking account, this article will equip you with the knowledge to navigate banking fees intelligently.

What is the Bank of America Core Checking Maintenance Fee?

The core checking maintenance fee is a standard charge imposed by Bank of America on certain checking accounts to cover the operational expenses of maintaining these accounts. This fee is part of the bank’s revenue model, allowing them to provide essential banking services while ensuring the sustainability of their operations.

Bank of America provides a range of checking account choices designed to suit the unique requirements of its clientele. Among these options, the core checking account is popular for individuals seeking a basic checking solution with essential features and benefits. However, it’s necessary to be aware of the core checking maintenance fee to avoid surprises or unexpected charges.

The core checking maintenance fee serves several purposes within the banking ecosystem. Firstly, it helps offset the costs associated with account maintenance, including administrative tasks, account management, and record-keeping. Bank of America invests significant resources in maintaining a robust banking infrastructure to ensure seamless account operations and provide quality customer service. The maintenance fee covers these operational expenses, enabling the bank to deliver a reliable banking experience to its customers.

Secondly, the core checking maintenance fee plays a role in the bank’s revenue generation. As a financial institution, Bank of America relies on various revenue streams to sustain its operations and drive profitability. While the core checking account may offer certain features and benefits to account holders, such as online banking, debit card access, and bill pay services, it’s essential to recognize that these services come with associated costs. The maintenance fee helps offset these costs and supports the bank’s ability to invest in technological advancements, product development, and customer service initiatives.

It’s worth noting that the core checking maintenance fee is a standard practice among many banks and financial institutions. The exact cost can differ based on account type, location, and usage, but the fundamental purpose remains unchanged throughout the industry.

Banks implement maintenance fees to cover the expenses of essential banking services and maintain a sustainable business model in an increasingly competitive market.

Exploring Bank of America’s Core Checking Account and Strategies to Avoid Monthly Maintenance Fees

Monthly Maintenance Fee

Bank of America’s Core Checking account has a monthly maintenance fee of $12.00. However, there are simple ways to bypass this fee each month or statement cycle:

- Qualifying Direct Deposit:

- Ensure you deposit $250 or more directly into your account at least once.

- Minimum Balance: Maintain an average daily balance of $1,500 or more in your Core Checking account.

- Student Waiver: Students under 23 years old enrolled in high school, college, or vocational programs are eligible for a fee waiver.

ATM Fees

Bank of America strives to offer convenience without hefty fees for ATM transactions:

- Bank of America ATMs: No fees for deposits, withdrawals, transfers, or balance inquiries.

- Non-Bank of America ATMs in the U.S.: A $2.50 fee, plus any charges from the ATM’s operator.

- Non-Bank of America ATMs outside the U.S.: A $5.00 fee, plus any charges from the ATM’s operator.

Overdraft Policy

Bank of America offers two options to manage overdrafts:

- Standard Option: Transactions are authorized even if they result in overdrafts, with a $35 Overdraft Item fee per transaction or a $35 Returned NSF fee for declined transactions.

- Decline-All Option: Transactions causing overdrafts are declined, with a $35 NSF fee per declined transaction.

- Emergency cash withdrawals at Bank of America ATMs may incur a $35 Overdraft Item fee if not covered by the end of the business day.

Extended Overdrawn Balance Charge

- If your account stays overdrawn for five consecutive business days (weekends excluded), there will be an extra charge of $35.00.

- Overdraft Protection: For a $12.00 transfer fee per transaction, you can set up Overdraft Protection. This automatically transfers available funds from a linked savings or second eligible checking account to cover potential overdrafts. Only one transfer fee is charged per day.

- Review your Schedule of Fees and Deposit Agreement for detailed information about your account terms and conditions.

Here’s a simple table outlining the maintenance fees for Bank of America Core Checking:

| Maintenance Fee Criteria | Monthly Maintenance Fee |

| Qualifying Direct Deposit of $250 or more | $0* |

| Keep a mean daily balance of at least $1,500. | $0* |

| Student Waiver (students under 23 enrolled in high school, college, or vocational program) | $0* |

| No qualifying criteria were met | $12.00 |

Fees are waived if qualifying criteria are met.

This table summarizes the monthly maintenance fee for Bank of America Core Checking and the requirements for fee waivers. Meeting any specified criteria results in a fee waiver, while not meeting any of them incurs a $12.00 monthly maintenance fee.

Why Does Bank of America Charge a Maintenance Fee?

Bank of America’s Core Checking maintenance fee is a standard charge levied on certain checking accounts to cover the operational expenses of maintaining these accounts. Exploring the intricacies of this charge is crucial for understanding its importance and its effects on individuals who hold accounts.

Rationale Behind the Fee

The maintenance fee serves as a means for Bank of America to offset the costs incurred in providing essential banking services to its customers. These costs encompass various operational activities, including account management, customer support, transaction processing, and infrastructure maintenance. Bank of America invests significant resources in maintaining a robust banking ecosystem to ensure the smooth functioning of its checking account offerings. This includes maintaining secure online and mobile banking platforms, staffing customer service centers, and adhering to regulatory compliance standards.

Costs Associated with Account Maintenance

Bank of America incurs various expenses in the day-to-day maintenance of checking accounts, which contribute to the justification for the maintenance fee. These expenses may include:

Administrative Costs

Checking accounts involves administrative tasks such as account setup, maintenance, and closure. Bank of America allocates resources to handle these administrative functions efficiently, including personnel costs, software licensing fees, and operational overhead.

Technology Investments

Bank of America continually invests in technology infrastructure to enhance the banking experience for its customers. This includes developing and maintaining secure online portals, mobile banking apps, and digital payment platforms. These technological investments incur ongoing maintenance costs, including software updates, cybersecurity measures, and server maintenance.

Customer Support Services

Ensuring prompt and efficient customer assistance is vital in fostering satisfaction and building long-term customer loyalty. Bank of America operates customer service centers with trained representatives to assist customers with account inquiries, dispute resolution, and technical support. The maintenance fee helps cover the expenses of these support services, including staff salaries, training programs, and call center infrastructure.

Regulatory Compliance

Banks are subject to stringent regulatory requirements to safeguard customer interests and maintain the financial system’s integrity. Bank of America dedicates resources to ensure compliance with regulatory standards, including implementing anti-money laundering measures, fraud detection systems, and privacy protections. These compliance efforts entail regulatory reporting, audits, and compliance personnel costs.

Importance of Fee Transparency

While the core checking maintenance fee is a standard practice in the banking industry, transparency is essential to fostering trust and confidence among account holders. Bank of America is committed to providing clear and comprehensive information about its fee structures, including the core checking maintenance fee. By transparently disclosing the fee’s rationale and associated costs, Bank of America aims to empower customers to make informed decisions about their banking relationships.

Qualifying Criteria for Fee Waivers and Discounts

While the core checking maintenance fee is a standard charge for most account holders, Bank of America offers various options for qualifying for fee waivers or discounts. Understanding these criteria and taking proactive steps to meet them can help you avoid paying the maintenance fee. Standard eligibility criteria for fee waivers may include:

- Maintaining a Minimum Balance: Many banks, including Bank of America, offer fee waivers to customers who maintain a minimum daily balance in their core checking accounts. Ensuring your account balance remains above the specified threshold allows you to qualify for the fee waiver and avoid the maintenance fee.

- Direct Deposit Requirement: Another common requirement for fee waivers is setting up direct deposit into your core checking account. Bank of America may offer fee waivers to customers with recurring direct deposits, such as paychecks or government benefits, credited to their account each month.

- Student and Military Benefits: Students and military members may be eligible for unique banking benefits, including fee waivers for core checking maintenance fees. Bank of America offers specific programs tailored to students and military personnel, allowing them to avoid particular fees.

- Account Linking: Some banks allow customers to link multiple accounts or maintain a certain level of relationship with the bank to qualify for fee waivers. By connecting your core checking account with other BoA accounts or supporting a broader relationship with the bank, you may be eligible for fee waivers or discounts.

Tips and Strategies to Avoid the Core Checking Maintenance Fee

Apart from satisfying the eligibility requirements for fee exemptions, there are various proactive approaches you can employ to steer clear of the core checking maintenance fee:

- Opt for Paperless Statements: Many banks offer incentives for paperless statements, including fee waivers for specific account maintenance fees. You can often qualify for fee waivers or discounts by receiving statements electronically instead of by mail.

- Explore Alternative Account Options: If you find that you’re unable to meet the criteria for fee waivers on your current core checking account, consider exploring alternative account options offered by Bank of America. BoA may have other checking account products with different fee structures or eligibility requirements that better suit your financial situation.

- Review Account Activity Regularly: Monitoring your account activity regularly can help you identify any potential fees or charges before they’re assessed. By staying informed about your account balance, transactions, and fee waivers, you can take proactive steps to avoid unnecessary fees.

- Utilize Online and Mobile Banking Tools: Bank of America provides comprehensive online and mobile banking services, enabling users to oversee their accounts efficiently. Through these platforms, individuals can easily monitor account activity, establish alerts, and track expenses, empowering them to manage their finances and prevent unforeseen charges effectively.

Benefits of Bank of America Core Checking

The Bank of America Core Checking account offers several benefits designed to meet the diverse financial needs of its customers. Here are some key benefits of the Core Checking account:

Accessibility

Access to a vast network of Bank of America branches and ATMs nationwide, providing convenient banking services wherever you are. Online and mobile banking systems allow individuals to oversee accounts, settle bills, move money, and remotely deposit checks.

Flexibility

You don’t need a specific amount of money to open the account, so it suits people with different financial circumstances. Option to link other Bank of America accounts for easy fund transfers and account management.

Convenience

Free access to Bank of America ATMs for deposits, withdrawals, transfers, and balance inquiries. Option to set up direct deposit for easy and seamless paycheck deposits.

Security

Bank of America’s robust security measures, including encryption technology and fraud monitoring, help safeguard your account against unauthorized access and fraudulent activity.

Additional Features

Option to enroll in overdraft protection to prevent declined transactions and avoid overdraft fees. It is compatible with Zelle® for quick and secure money transfers between friends and family.

Student Benefits

Students under 23 enrolled in high school, college, or vocational programs may qualify for a monthly maintenance fee waiver, making banking more affordable.

Customer Support

Access to Bank of America’s dedicated customer service team for assistance with account inquiries, technical support, and dispute resolution.

Overall, the Bank of America Core Checking account provides a combination of accessibility, flexibility, and security, making it a convenient and reliable option for individuals seeking essential banking services. Whether you’re handling your everyday finances or strategizing for the future, the Core Checking account comes with functionalities aimed at streamlining your banking interactions and supporting you in reaching your financial objectives.

How to Set Up Overdraft Protection

Setting up Overdraft Protection with Bank of America is a straightforward process that can provide peace of mind by helping to prevent declined transactions and avoid overdraft fees. Here’s how you can set it up:

- Log In to Online Banking: You have the option to access your Bank of America account either through their online banking portal or their mobile app. This involves inputting your username and password.

- Navigate to the Overdraft Protection Section: Once logged in, navigate to the section of your account dashboard or settings menu that pertains to overdraft protection. This section may be labeled differently depending on the specific layout of the online banking platform but is typically found within the account management or settings options.

- Review Overdraft Protection Options: Bank of America typically offers several options for overdraft protection, including linking a savings account, credit card, or second eligible checking account. Review the available options to determine which one best suits your needs.

- Select Preferred Option: Choose the option you prefer for overdraft protection. If you prefer to link a savings account or a second eligible checking account, you may need to provide the account details for the account you wish to link.

- Authorize Transfer and Confirm: Follow the prompts to authorize the transfer of funds from your linked account to cover potential overdrafts. Depending on your option, you may be prompted to specify the funds you want to designate for overdraft protection.

- Review Terms and Conditions: Before finalizing the setup process, review the terms and conditions associated with overdraft protection to ensure you understand any applicable fees or limitations.

- Confirm and Save Settings: Once you’ve reviewed and confirmed your selections, save your settings to activate overdraft protection on your account.

- Monitor Account Activity: After setting up overdraft protection, monitor your account activity regularly to ensure it meets your financial needs and preferences. Review and adjust your overdraft protection settings as needed periodically.

Following these steps, you can set up Overdraft Protection with Bank of America to help manage your account more effectively and avoid potential overdraft fees. If you have any questions or need assistance during the setup process, don’t hesitate to contact Bank of America’s customer service for support.

Key Takeaways:

- Understanding Bank of America’s Core Checking Maintenance Fee: The monthly maintenance fee is a standard charge for maintaining a Core Checking account.

- Fee Avoidance Strategies: You can avoid the maintenance fee by fulfilling specific requirements, like keeping a minimum balance or arranging direct deposits.

- ATM Fee Structure: Bank of America offers fee-free transactions at its ATMs and provides transparent fee schedules for non-Bank of America ATM usage.

- Overdraft Policies: Bank of America offers options for managing overdrafts, including standard and decline-all options and overdraft protection services.

- Student Benefits: Students under 23 years old enrolled in qualifying programs may be eligible for fee waivers.

- Benefits of Bank of America Core Checking: The Core Checking account offers accessibility, flexibility, security, and additional features tailored to meet customers’ financial needs.

Additional Resources:

- Bank of America’s official website details its checking account options, fees, and policies.

- The Personal Schedule of Fees and Deposit Agreement outlines the specific terms and conditions associated with the Core Checking account.

- Customer service representatives at Bank of America branches or via phone can provide assistance and clarification on account-related inquiries.

- Online banking platforms and mobile apps offer access to account information, fee schedules, and tools for managing finances on the go.

Conclusion

Understanding banking fees might seem overwhelming, but armed with the right information and approaches, you can efficiently handle your finances and steer clear of unwarranted expenses. By understanding the core checking maintenance fee structure, qualifying criteria for fee waivers, and implementing proactive strategies, you can minimize or eliminate the impact of fees on your Bank of America core checking account. Remember to stay informed, monitor your account regularly, and explore all available options to make the most of your banking experience.

Debunking the Top 5 Budget Myths That Keep You Broke: A Guide to Financial Freedom

Navigating the terrain of budgeting can often feel like an overwhelming chore in the maze of personal finance. Despite our best efforts, many of us are caught in a vicious cycle of overspending, mounting debt, and stressful financial situations. Why does this occur? The widespread misconceptions about budgeting that frequently mislead us could hold the key to the solution.

In this extensive tutorial, we’ll dispel the top five financial fallacies that keep you broke. By dispelling these myths, we aim to arm you with the information and resources you need to take charge of your financial destiny and realize long-term success.

What are Myths?

Myths are traditional stories or narratives that are often passed down through generations. They typically involve supernatural beings, gods, heroes, or legendary events and are frequently used to explain natural phenomena, cultural practices, or societal values. Myths can be found in every culture around the world and serve various purposes, including teaching moral lessons, preserving cultural heritage, and providing explanations for the mysteries of the world.

In a broader sense, myths can also refer to widely held beliefs or misconceptions that are not necessarily based on factual evidence but are perpetuated through cultural or social influence. These contemporary myths include false beliefs about anything from history and science to personal finance, health, and much more. Debunking these myths often involves providing accurate information and challenging commonly held beliefs that may not be supported by evidence or logic.

| Myth | Reality |

| “I don’t have time to budget.” | Budgeting is a worthwhile investment of time that can lead to greater financial control and security. It becomes easier with practice and offers long-term benefits. |

| Making a budget can be difficult, particularly if you’re not good with numbers. | Budgeting doesn’t require advanced math skills. Basic arithmetic suffices and user-friendly tools are available to simplify the process for those who dislike math. |

| “Budgeting is boring.” | While it may seem tedious at first, budgeting is crucial for financial success and can lead to greater freedom and peace of mind. |

| “I can do a budget in my head.” | While mental budgeting is impressive, most people benefit from a tangible budget that they can track and adjust as needed. Collaboration with a partner can enhance its effectiveness. |

| “I manage my finances by monitoring and recording all of my expenses.” | Tracking expenses is a valuable practice, but it’s not a substitute for comprehensive budgeting. A well-rounded budget considers future goals and provides a roadmap for financial success. |

Myth 1: Budgeting is Restrictive and Confining

One of the most prevalent myths surrounding budgeting is the belief that it imposes strict limitations on your spending habits, stifling your ability to enjoy life to the fullest. However, the truth is quite the opposite. A well-crafted budget serves as a roadmap to financial freedom, offering clarity and direction in achieving your financial goals.

Debunking Myth 1

- Budgeting does not mean deprivation; instead, it empowers you to allocate your resources intentionally, prioritizing what truly matters to you.

- By monitoring your spending and pinpointing areas where you can reduce or redistribute funds, you empower yourself to make mindful choices about how you allocate your resources towards experiences and items that truly enrich your life.

- Budgeting encourages mindfulness and responsible decision-making, leading to greater financial security and peace of mind.

Myth 2: Budgeting Requires Sacrificing Your Lifestyle

Another common misconception is that budgeting necessitates sacrificing your current lifestyle in favor of future financial stability. While it’s true that budgeting involves making informed trade-offs, it doesn’t mean giving up the things that make life enjoyable.

Debunking Myth 2

- Budgeting is about aligning your spending with your values and priorities.

- Understanding your core values enables you to effectively distribute your resources towards nurturing the lifestyle you aspire to achieve.

- Rather than viewing budgeting as a constraint, think of it as a tool for maximizing your resources and optimizing your enjoyment.

- You have the power to prioritize your spending deliberately, ensuring that you can enjoy the things that genuinely bring you joy while also making progress towards your future financial objectives.

- With careful planning and foresight, budgeting allows you to strike a balance between living well today and building a secure future for tomorrow.

Myth 3: Budgeting is Too Complicated and Time-Consuming

Many people shy away from budgeting because they perceive it as a complex and time-consuming endeavor. However, modern budgeting tools and techniques have made the process more accessible and efficient than ever before.

Debunking Myth 3

- Budgeting doesn’t have to be complicated. With the plethora of user-friendly apps and software available, you can create and manage a budget with minimal effort.

- Automating your finances, such as setting up recurring payments and savings contributions, streamlines the budgeting process and reduces the need for manual intervention.

- Allocating a few minutes every week to scrutinize your budget and monitor your spending can help you gain a substantial understanding of your financial patterns and make well-informed choices.

Myth 4: Budgeting is Only for People with High Incomes

Another common myth is that budgeting is only necessary for those with high incomes or significant financial assets. In reality, budgeting is a fundamental tool for anyone looking to manage their money effectively, regardless of their income level.

Debunking Myth 4

- Budgeting is not about how much money you make; it’s about how you choose to allocate and manage your resources. Regardless of your income, budgeting can help you make the most of what you have and work toward your financial goals.

- In fact, budgeting is essential for those with limited incomes, as it can help stretch each dollar further and ensure that basic needs are met without overspending.

- By taking a proactive approach to budgeting, even people with modest incomes can accumulate money, attain financial stability, and eventually escape the pattern of living paycheck to paycheck.

Myth 5: Budgeting is One-Size-Fits-All

Some individuals may be deterred from budgeting because they believe it requires conforming to a rigid set of rules or guidelines that don’t align with their unique circumstances. However, the beauty of budgeting lies in its flexibility and adaptability to your individual needs and preferences.

Debunking Myth 5

- There is no one-size-fits-all approach to budgeting.

- Crafting a budget that aligns with your unique financial objectives, lifestyle choices, and personal principles is essential.

- Whether you prefer a detailed spreadsheet or a simple pen-and-paper method, the key is to find a budgeting system that works for you and fits seamlessly into your life.

- As your circumstances change over time, your budget can evolve with you. Regularly reassessing your financial goals and adjusting your budget accordingly ensures that it remains relevant and effective in helping you achieve financial success.

Practical Budgeting Myths

Here are some practical budgeting tips to help you manage your finances effectively:

Track Your Expenses

Begin by documenting every expense you incur over a month. This includes everything from significant bills to small purchases like coffee or snacks. Use a notebook, spreadsheet, or budgeting app to keep track of where your money is going.

Create a Budget

Based on your expense tracking, create a budget that outlines your income and expenses. Allocate specific amounts for essentials like rent or mortgage payments, utilities, groceries, transportation, and savings. Be realistic and flexible in your budgeting approach.

Set Financial Goals

Establish both short- and long-term financial objectives, such as debt repayment, emergency fund accumulation, vacation savings, and retirement investment. Setting and meeting specific goals will help you stay within your budget and make wiser financial choices.

Prioritize Saving

Make budgeting for savings a top priority. Try setting aside some money every month, even if it’s just a tiny bit. Consider arranging automatic transfers from your checking account to a savings or investment account to simplify your saving routine.

Monitor and Adjust

Review your budget and track your spending regularly to ensure you’re staying on track. If you notice areas where you’re overspending or underspending, adjust your budget accordingly. Take the initiative to solve any arising financial issues.

Use Cash Envelopes

Consider using the cash envelope method for your flexible spending areas, such as eating out, going to movies or events, or buying clothes. At the beginning of the month, allocate a specific amount of cash to each envelope and only spend what’s available in each envelope.

Reduce Unnecessary Expenses

Look for ways to cut back on non-essential expenses to free up more money for savings or debt repayment. This could include dining out less frequently, canceling unused subscriptions, or finding cheaper alternatives for goods and services.

Plan for Irregular Expenses

Allocate funds into a designated savings account to prepare for unexpected expenses such as vehicle maintenance, medical costs, or seasonal holiday expenditures. Having a separate fund for these expenses can ensure they are within your budget.

Stay Flexible

Life can be full of surprises, including unforeseen expenses or income fluctuations. It’s important to remain adaptable and ready to modify your budget when necessary to adapt to these shifts. Maintaining an emergency fund can offer a financial cushion during difficult periods.

Seek Professional Advice if Needed

If you need help managing your finances or making progress toward your financial goals, consider seeking advice from a financial advisor or counselor. They can offer you individualized advice and methods to assist you in overcoming a dire economic situation.

50/30/20 Rule

A widely accepted guideline for budgeting is the 50/30/20 Rule, which states that individuals should divide their income after taxes into three main categories: savings, flexible spending, and necessities.

Here’s a breakdown of the Rule:

50% for Needs

Dedicate half of your income after taxes to cover essential expenses or necessities. These are expenses that are necessary for your basic living requirements, such as housing (rent or mortgage payments), utilities, groceries, transportation, insurance premiums, minimum debt payments, and healthcare costs. This category covers expenses that you can only quickly eliminate or significantly reduce that impact your quality of life.

30% for Wants

Dedicate 30% of your after-tax income to discretionary spending or wants. These are expenses that enhance your lifestyle or provide enjoyment but are not essential for survival. Examples include dining out, entertainment, travel, hobbies, clothing beyond necessities, and non-essential subscriptions or memberships. This category allows for flexibility and enjoyment in your budget without overspending.

20% for Savings and Debt Repayment

Reserve 20% of your after-tax income for savings, investments, and debt repayment. This category includes contributions to emergency savings, retirement accounts (such as 401(k) or IRA), investments in stocks or mutual funds, and accelerated debt payments beyond the minimum required. Building a robust savings cushion and reducing debt are essential steps towards achieving financial security and long-term wealth accumulation.

The rule offers a straightforward approach to financial management and budgeting. It highlights the significance of allocating funds wisely across long-term savings, discretionary expenses, and essential expenditures. While it might only suit some people’s financial needs or objectives, it serves as a helpful foundation for crafting a budget that reflects your priorities and principles. Flexibility is critical, allowing for adjustments according to individual situations, like increased housing expenses or specific saving targets. The key is to find a budgeting approach that works for you and supports your financial well-being.

Uses of Emergency Fund

As a safety net for unforeseen costs or unexpected financial difficulties, an emergency fund is an essential part of managing one’s finances. It is a pool of money set aside expressly for unforeseen circumstances that may disrupt your regular income or require immediate attention. Here are some critical aspects of emergency funds:

Purpose

Having an emergency fund is primarily intended to provide a sense of security and stability in the event of unanticipated events. It serves as a form of financial protection for unexpected situations like sudden medical emergencies, vehicle repairs, unemployment, home maintenance, or any other unforeseen expenses. Maintaining an emergency fund enables you to navigate these situations without relying on costly loans or draining savings designated for different purposes.

Size

The amount you should set aside for your emergency fund varies depending on factors such as your monthly spending, your income stability, the security of your job, and how much risk you’re comfortable with. Financial experts commonly recommend maintaining savings that cover living expenses for a period ranging from three to six months as a general rule of thumb. However, individuals with more volatile income streams or higher risk factors may opt to save a larger emergency fund, while others may feel comfortable with a smaller cushion.

Location

Emergency funds need to be readily available during crises, so it’s crucial to keep them in an easily accessible and low-risk account. Consider putting your emergency funds in a money market account, high-yield savings account, or other dedicated savings account that isn’t connected to your everyday spending funds. While it’s essential to earn some interest on your emergency fund, prioritizing liquidity and stability is paramount.

Building an Emergency Fund

Establishing an emergency fund demands dedication and regularity. Begin by determining a precise savings objective tied to your monthly expenditures, then steadily strive to achieve it. Dedicate a portion of your earnings to your emergency fund every month until you’ve amassed the intended sum. It’s wise to automate contributions to your emergency fund to maintain consistency and resist the urge to use the funds for other purposes.

Maintaining and Replenishing

Once you’ve established an emergency fund, it’s essential to periodically review and reassess your savings goals, especially as your financial situation changes. If you use your emergency fund to address unforeseen costs, it’s crucial to prioritize replenishing it promptly. This ensures that the fund remains available for its intended purpose and retains its effectiveness in providing financial security.

Differentiation from Other Savings

It’s important to distinguish your emergency fund from other savings goals or accounts, such as retirement savings, investment accounts, or short-term savings, for specific goals like vacations or home purchases. While these accounts serve essential purposes, they should not be used interchangeably with your emergency fund, as doing so may compromise your financial security in times of need.

Overall, an emergency fund is a fundamental tool for financial resilience and stability. By prioritizing savings and building a robust emergency fund, you can better withstand unexpected challenges and navigate financial uncertainties with confidence and peace of mind.

Key Takeaways:

- Budgeting is crucial in managing personal finances, serving as a cornerstone for managing earnings and expenditures and reaching financial objectives.

- Common budgeting myths, such as the belief that budgeting is restrictive or time-consuming, can hinder financial success. Dispelling these myths is crucial for adopting effective budgeting practices.

- Practical budgeting tips include tracking expenses, creating a budget, setting financial goals, prioritizing saving, monitoring and adjusting your budget, reducing unnecessary costs, planning for irregular expenses, staying flexible, and seeking professional advice if needed.

- A well-known budgeting guideline is the 50/30/20 Rule, which suggests allocating after-tax income into three categories: 50% for necessities, 30% for wants, and 20% for debt repayment and savings.

- Emergency funds are essential financial safety nets designed to cover unexpected expenses or financial emergencies. They should be easily accessible, liquid, and separate from other savings accounts.

- Creating and upkeeping an emergency fund demands commitment, regularity, and occasional evaluation to safeguard financial stability and tranquility.

FAQs

What is budgeting, and why is it important?

Budgeting is the process of creating a plan to manage income and expenses. It is essential for achieving financial goals, controlling spending, and building financial security.

How can I create a budget?

You can make a budget by tracking your expenses, categorizing them into needs and wants, setting financial goals, allocating funds accordingly, and monitoring your spending regularly.

What is the 50/30/20 Rule?

It is a budgeting principle that recommends that individuals allocate 50% of their post-tax income to essential expenses, 30% to discretionary spending, and 20% to savings and debt repayment.

What is an emergency fund, and why do I need one?

An emergency fund is a financial reserve designated to handle unforeseen expenses or sudden financial crises. It’s crucial for ensuring economic stability and offering reassurance during unexpected hardships.

How much should I save in an emergency fund?

Financial experts frequently recommend that people establish an emergency fund capable of covering their basic living expenses for 3 to 6 months. However, the ideal amount may differ depending on personal situations and factors like risk tolerance.

Additional Resources:

- “The Total Money Makeover^” by Dave Ramsey – This book offers practical advice on budgeting, saving, and achieving financial freedom.

- “Your Money or Your Life^,” co-authored by Vicki Robin and Joe Dominguez, delves into the intricate connection between money and personal values, offering valuable perspectives on budgeting and achieving financial independence.

- “The Automatic Millionaire^” by David Bach – This book introduces the concept of automatic saving and budgeting to achieve financial goals effortlessly.

- EveryDollar – The budgeting app is recommended for those who prefer a user-friendly approach to budgeting.

- Mint – Personal finance app that helps users track expenses, set financial goals, and create budgets.

Conclusion

In conclusion, the journey to financial freedom begins with dispelling the myths that keep us trapped in cycles of economic insecurity. By debunking the top 5 budget myths outlined in this guide, you can take the first step toward reclaiming control of your finances and building a brighter future.

Remember, budgeting is not about deprivation or sacrifice; it’s about empowerment and freedom. By embracing a proactive approach to budgeting and making informed decisions about your money, you can break free from the constraints of financial uncertainty and chart a course toward lasting prosperity.

Dave Ramsey’s Guide to Saving, Giving, and Spending Percentages

A strong plan and methodical execution are necessary for obtaining financial success and stability in the area of personal finance. Famous financial counselor Dave Ramsey has long been a source of inspiration for people trying to take charge of their economic destiny. A core tenet of Ramsey’s philosophy is the division of income among three categories: savings, giving, and spending. We explore Dave Ramsey’s suggested percentages for saving, sharing, and spending in this extensive guide, providing you with tactics and insights to help you confidently manage your finances.

Understanding Dave Ramsey’s Philosophy

At the core of Dave Ramsey’s financial philosophy lies the principle of stewardship—responsibly managing the resources entrusted to us. Ramsey emphasizes the importance of living within one’s means, avoiding debt, and building wealth through intentional decisions and disciplined habits. Central to his approach is the concept of allocating income into distinct categories to ensure a balanced and purposeful use of financial resources.

Saving Percentage